While we aim for the highest quality standards, management may not always prioritize quality to the same extent as quality costs. This raises important questions about the cost of quality and an even more crucial issue – what is the cost of neglecting it?

Every organization should focus on determining the extent to which its resources are used to prevent poor quality. This includes evaluating product quality and addressing internal and external errors. Having this information allows the organization to determine potential savings that can be achieved by implementing process improvements.

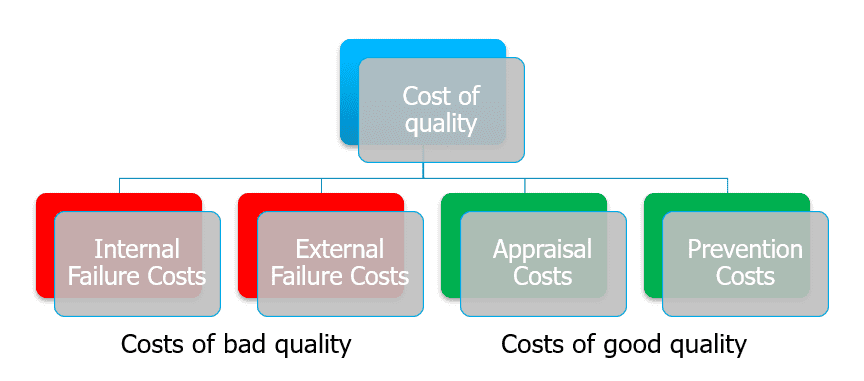

Cost of Quality – Structure and Analysis

Quality costs can be divided into two categories: low (bad) and good quality. The former will include the costs of internal and external problems. The costs of bad quality, which are part of the quality costs, are waste, so focusing on its reduction is crucial to the financial improvement of the company. Why? Because they account for 20 to 40% of the annual cost of manufactured parts.

Internal Failure Costs

These costs result from deficiencies identified before the product is delivered to the customer. These include:

– non-compliant parts classified as scrap

– rework

– internal selection, i.e. repeated checking of products in work-in-progress production or in the finished products warehouse

– unplanned downtime

– machine repairs

– lack of subcomponents included in the finished product

– passing components through the production process again to recover parts after disassembly.

External Failure Costs

External costs occur after the customer receives the product and include costs related to:

– handling quality complaints. It’s important to note that some customers initially charge the supplier with administrative costs merely for submitting a complaint in the system. Moreover, there is a growing trend where customers consider the costs associated with complaint-related handling. What exactly does this entail?

If operators need to remove a non-compliant component from the vehicle, they will incur man-hours charges.

When measurements are carried out on a suspicious part, we may be charged for the man-hours of the person carrying out the measurements.

This same applies to the selection of incoming area components. In addition to paying the sorting company for the selection performed, we may also receive a charge from the customer for moving containers with parts by a forklift.

Additionally, the production plant (0-km) and service parts distribution centers divide the cost of quality into their respective incurred expenses. In the second scenario, we apply it when we replace components at dealer stations after detecting a problem or after repairing the vehicle due to damage.

– warranty returns. warranty returns, with particular attention given to the NTF (No Trouble Found) process. More information on this process can be found in a separate article.

– an escalation activity involves the official selection of components assembled into vehicles and blocked at the shipping yard, typically carried out to address urgent quality issues or customer complaints called Yard Hold.

What else?

– Costs associated with recovering funds from sub-suppliers due to quality issues identified internally or externally. While theoretically, we should recoup 100% of the costs resulting from sub-supplier faults, in reality, we often encounter various complexities. If challenges arise during the cost recovery process, it’s advisable to involve central departments.

– Costs related to handling special audits conducted by both the client’s representative and the Certification Body. This situation occurs when an organization faces special scrutiny due to quality or logistical issues.

Fig. 1. Costs breakdown

Cost of Good Quality

This category encompasses preventive and appraisal costs.

Prevention Costs

Prevention costs involve making investments to avert quality deficiencies and nonconformities before delivering products to the customer. They include activities such as quality planning, project reviews, process control, training, and quality audits, including those conducted at suppliers (e.g., VDA 6.3).

While these preventive measures may seem extensive, the repercussions of failures occurring later in production can lead to significantly higher costs. Therefore, it’s essential to prioritize the detection of non-compliant components as early as possible, preferably at the supplier stage, as the costs incurred at this phase are typically lower than those associated with handling official complaints.

Appraisal Costs

Appraisal costs encompass expenditures related to determining the degree of compliance with quality requirements. This includes costs associated with:

– Tests

– Inspections conducted during the manufacturing process

– Inspection of components at the incoming inspection stage

– Product audits

– Calibration

– Maintenance of measurement devices

– Requalification tests mandated by the IATF 8.6.2 standard and most customers as part of their specific requirements

– Periodic training for employees, such as process auditors according to VDA 6.3.

Invest in Prevention – a Strategy for Optimizing Quality Costs

While the array of costs may appear daunting, there are avenues for cost reduction. The cornerstone of this approach is investment in prevention costs. By mitigating potential issues and implementing robust controls, organizations can curtail both internal and external problem costs. Quality assurance inevitably entails expenses, but it’s imperative that these expenditures are strategically directed towards prevention.

{kind=link}

{kind=link}